AutoML with AutoGluon for Timeseries Forecasts

- Part 1: AutoML with AutoGluon for Tabular Data

- Part 2: AutoML with AutoGluon for Multi-Modal Data

- Part 3: AutoML with AutoGluon for Timeseries Forecasts

AutoGluon automates machine learning tasks enabling you to easily achieve strong predictive performance in your applications. With just a few lines of code, you can train and deploy high-accuracy machine learning and deep learning models on image, text, time series, and tabular data.

- AutoML with AutoGluon for Timeseries Forecasts

Installation

Installing AutoGluon with GPU support:

pip install -U pip

pip install -U setuptools wheel

pip install torch==1.13.1+cu117 torchvision==0.14.1+cu117 --extra-index-url https://download.pytorch.org/whl/cu117

pip install autogluon

# for visualizations

pip install bokeh==2.0.1"

Single Variate Forecasting

# get dataset

!wget https://raw.githubusercontent.com/databricks/Spark-The-Definitive-Guide/master/data/retail-data/all/online-retail-dataset.csv -P dataset

from autogluon.timeseries import TimeSeriesDataFrame, TimeSeriesPredictor

import matplotlib.pyplot as plt

from datetime import datetime as dt

import pandas as pd

import seaborn as sns

SEED = 42

MODEL_PATH = 'model'

Data Preprocessing

df = pd.read_csv('dataset/online-retail-dataset.csv')

df.head(5)

| InvoiceNo | StockCode | Description | Quantity | InvoiceDate | UnitPrice | CustomerID | Country | |

|---|---|---|---|---|---|---|---|---|

| 0 | 536365 | 85123A | WHITE HANGING HEART T-LIGHT HOLDER | 6 | 12/1/2010 8:26 | 2.55 | 17850.0 | United Kingdom |

| 1 | 536365 | 71053 | WHITE METAL LANTERN | 6 | 12/1/2010 8:26 | 3.39 | 17850.0 | United Kingdom |

| 2 | 536365 | 84406B | CREAM CUPID HEARTS COAT HANGER | 8 | 12/1/2010 8:26 | 2.75 | 17850.0 | United Kingdom |

| 3 | 536365 | 84029G | KNITTED UNION FLAG HOT WATER BOTTLE | 6 | 12/1/2010 8:26 | 3.39 | 17850.0 | United Kingdom |

| 4 | 536365 | 84029E | RED WOOLLY HOTTIE WHITE HEART. | 6 | 12/1/2010 8:26 | 3.39 | 17850.0 | United Kingdom |

df.info()

# <class 'pandas.core.frame.DataFrame'>

# RangeIndex: 541909 entries, 0 to 541908

# Data columns (total 8 columns):

# # Column Non-Null Count Dtype

# --- ------ -------------- -----

# 0 InvoiceNo 541909 non-null object

# 1 StockCode 541909 non-null object

# 2 Description 540455 non-null object

# 3 Quantity 541909 non-null int64

# 4 InvoiceDate 541909 non-null object

# 5 UnitPrice 541909 non-null float64

# 6 CustomerID 406829 non-null float64

# 7 Country 541909 non-null object

# dtypes: float64(2), int64(1), object(5)

# memory usage: 33.1+ MB

# only sample last 10.000 items

# df_sample = df.iloc[-10000:]

# take all items

df_sample = df.copy()

# renaming columns

df_sample.rename(columns={'InvoiceNo': 'item_id', 'InvoiceDate': 'timestamp'}, inplace=True)

# create sale total price

df_sample['target'] = df_sample['Quantity'] * df_sample['UnitPrice']

df_sample['item_id'] = 'online_sales'

# create single variant timeseries

df_sample.drop(

['StockCode', 'Description', 'CustomerID', 'Country', 'Quantity', 'UnitPrice'],

axis=1, inplace=True)

df_sample.head(5)

| item_id | timestamp | target | |

|---|---|---|---|

| 0 | online_sales | 12/1/2010 8:26 | 20.40 |

| 1 | online_sales | 12/1/2010 8:26 | 27.80 |

| 2 | online_sales | 12/1/2010 8:26 | 2.60 |

| 3 | online_sales | 12/1/2010 8:26 | 5.85 |

| 4 | online_sales | 12/1/2010 8:26 | 19.90 |

# reformat timestamp to remove time from date

df_sample['timestamp'] = pd.to_datetime(df_sample['timestamp']).dt.strftime('%m/%d/%Y')

df_sample.head(5)

| item_id | target | timestamp | |

|---|---|---|---|

| 0 | online_sales | 16.6 | 12/23/2010 |

| 1 | online_sales | 8.5 | 12/23/2010 |

| 2 | online_sales | 20.8 | 12/23/2010 |

| 3 | online_sales | 20.8 | 12/23/2010 |

| 4 | online_sales | 20.8 | 12/23/2010 |

# groupby date and sum() up the sales

df_sample = df_sample.groupby(

['item_id', 'timestamp']).sum()

print(df_sample.info())

# MultiIndex: 305 entries, ('online_sales', '01/04/2011') to ('online_sales', '12/23/2010')

df_sample.head(5)

| item_id | timestamp | target |

|---|---|---|

| online_sales | 01/04/2011 | 15584.29 |

| 01/05/2011 | 75076.22 | |

| 01/07/2011 | 81417.78 | |

| 01/09/2011 | 32131.53 |

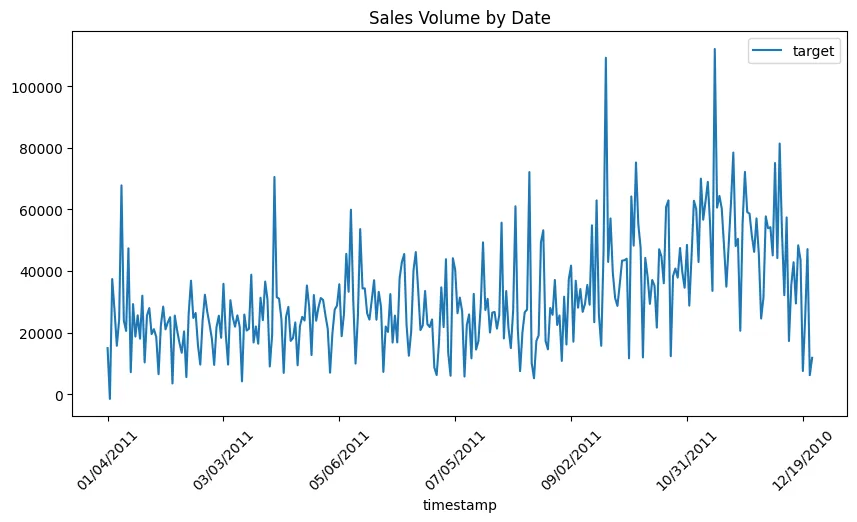

df_sample.loc['online_sales']['target'].plot(

title='Sales Volume by Date',

figsize=(10,5),

rot=45,

legend=True

)

plt.savefig('assets/AutoGluon_AutoML_TimeSeries_01.webp', bbox_inches='tight')

df_sample.to_csv('dataset/single_variant_ts.csv', index=True)

Model Training

ValueError: Frequency not provided and cannot be inferred. This is often due to the time index of the data being irregularly sampled. Please ensure that the data set used has a uniform time index, or create the

TimeSeriesPredictorsettingignore_time_index=True.

AutoGluon does not like irregular timeseries AT ALL... I manually fixed the timestamp column with regular, daily interval. Docs recommend auto-filling for missing data before model training.

train_data = TimeSeriesDataFrame('dataset/single_variant_ts.csv')

train_data.describe()

| target | |

|---|---|

| count | 305.000000 |

| mean | 31959.829292 |

| std | 17414.261664 |

| min | -1566.230000 |

| 25% | 20728.140000 |

| 50% | 27978.410000 |

| 75% | 42912.400000 |

| max | 112141.110000 |

# create a predictor for 30 days (30 row in dataset) forcast

sv_predictor = TimeSeriesPredictor(

prediction_length=30,

path=MODEL_PATH,

target='target',

eval_metric='sMAPE'

)

sv_predictor.fit(

train_data,

time_limit=800,

presets="medium_quality"

)

# Training complete. Models trained: ['Naive', 'SeasonalNaive', 'Theta', 'AutoETS', 'RecursiveTabular', 'DeepAR', 'WeightedEnsemble']

# Total runtime: 146.36 s

# Best model: WeightedEnsemble

# Best model score: -0.2301

sv_predictor.fit_summary()

Estimated performance of each model:

| model | score_val | pred_time_val | fit_time_marginal | fit_order | |

|---|---|---|---|---|---|

| 0 | WeightedEnsemble | -0.321595 | 1.042651 | 1.881647 | 7 |

| 1 | RecursiveTabular | -0.321595 | 1.042651 | 0.757291 | 5 |

| 2 | DeepAR | -0.384756 | 0.095033 | 69.751811 | 6 |

| 3 | AutoETS | -0.385364 | 22.865800 | 0.012004 | 4 |

| 4 | Theta | -0.397785 | 24.269135 | 0.009619 | 3 |

| 5 | SeasonalNaive | -0.403544 | 5.162711 | 0.010179 | 2 |

| 6 | Naive | -0.403544 | 5.572433 | 0.009085 | 1 |

| Number of models trained: 7 | |||||

| Types of models trained: | |||||

{'MultiWindowBacktestingModel', 'TimeSeriesGreedyEnsemble'} |

Model Evaluation

# return a 1 month forcast on the training data

sv_predictions = sv_predictor.predict(train_data, random_seed=SEED)

sv_predictions

| mean | 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| item_id | timestamp | ||||||||||

| online_sales | 2011-10-16 | 35231.549892 | 14821.287291 | 21889.080854 | 26885.810628 | 31139.108555 | 35389.176845 | 39525.311786 | 43747.076754 | 48715.574839 | 55619.827997 |

| 2011-10-17 | 37319.098400 | 9315.489680 | 18992.518673 | 25927.428089 | 31800.990269 | 37256.964611 | 42685.962390 | 48685.278476 | 55741.918605 | 65278.986905 | |

| 2011-10-18 | 38623.633612 | 5142.371285 | 16610.764052 | 24909.974641 | 32018.253338 | 38569.692694 | 45201.922577 | 52390.855571 | 60646.930906 | 72387.928409 | |

| 2011-10-19 | 40741.301758 | 1946.154973 | 15539.068760 | 25137.953113 | 33223.044572 | 40765.606934 | 48463.165389 | 56628.990736 | 66077.743741 | 79722.836483 | |

| 2011-10-20 | 49296.101707 | 6303.232915 | 21458.815514 | 31910.941266 | 40964.792632 | 49394.712059 | 57908.461563 | 66841.601504 | 77474.686240 | 92186.915812 | |

| 2011-10-21 | 42399.179004 | -4222.418692 | 11966.114749 | 23324.147218 | 33287.622759 | 42457.754199 | 51587.049946 | 61400.403661 | 72842.296970 | 88931.093472 | |

| 2011-10-22 | 33619.926637 | -17087.154419 | 364.144617 | 12901.404480 | 23491.862364 | 33662.238893 | 43520.884464 | 54164.964907 | 66630.573647 | 84037.471194 | |

| 2011-10-23 | 39042.384772 | -14703.540432 | 3853.552955 | 17218.430626 | 28519.710014 | 39090.598639 | 49763.392538 | 60939.668264 | 74324.111121 | 92676.374673 | |

| 2011-10-24 | 37314.733017 | -19270.824930 | 233.744114 | 14092.680263 | 26011.109933 | 37258.663681 | 48286.522116 | 60254.494754 | 74152.628169 | 93725.394967 | |

| 2011-10-25 | 40035.277581 | -19730.031575 | 823.364529 | 15754.378083 | 28379.185360 | 40095.125237 | 51768.504080 | 64369.746415 | 78969.545369 | 99392.125068 | |

| 2011-10-26 | 43809.551647 | -18581.300915 | 2831.155428 | 18233.929143 | 31493.221895 | 43799.325572 | 56059.960500 | 69262.074053 | 84846.687611 | 106247.592685 | |

| 2011-10-27 | 40978.233969 | -24604.018712 | -2246.682396 | 14204.335705 | 28124.915072 | 41120.107016 | 53865.685435 | 67632.214997 | 83850.112737 | 106498.851884 | |

| 2011-10-28 | 41743.192227 | -26024.978536 | -2645.385307 | 14166.811130 | 28273.284258 | 41561.178311 | 54943.112404 | 69180.700278 | 86004.451402 | 109515.329421 | |

| 2011-10-29 | 38315.939169 | -32037.733749 | -7961.047361 | 9530.292590 | 24433.420394 | 38430.213583 | 52199.831968 | 67014.321833 | 84580.597330 | 108781.710477 | |

| 2011-10-30 | 40790.730787 | -31714.294692 | -6632.032918 | 11250.135692 | 26624.395493 | 40830.333814 | 55083.397136 | 70254.854690 | 88116.212266 | 113018.777994 | |

| 2011-10-31 | 39601.428364 | -35269.325656 | -9299.692907 | 9073.426874 | 24982.993094 | 39702.658833 | 54402.247423 | 70171.210127 | 88614.257154 | 114229.722423 | |

| 2011-11-01 | 43321.091336 | -33495.290752 | -7238.416761 | 11718.451027 | 27982.345746 | 43267.875515 | 58529.011730 | 74809.030961 | 93805.173651 | 120492.849400 | |

| 2011-11-02 | 39873.310897 | -39638.237188 | -12259.488831 | 7259.635658 | 24107.774345 | 39944.400252 | 55573.550817 | 72172.974172 | 91871.915068 | 119270.200045 | |

| 2011-11-03 | 38897.212691 | -42509.220460 | -14725.370733 | 5465.492686 | 22784.085743 | 38756.254195 | 54814.426553 | 72198.679766 | 92621.915745 | 120534.229094 | |

| 2011-11-04 | 45310.748490 | -37919.694783 | -9357.164960 | 11175.946162 | 28815.300995 | 45152.634721 | 61626.068300 | 79239.016639 | 99980.063552 | 128811.104239 | |

| 2011-11-05 | 40524.113111 | -45095.463685 | -15760.925828 | 5668.926472 | 23679.488279 | 40503.121411 | 57398.500638 | 75497.467474 | 96633.997752 | 126117.225307 | |

| 2011-11-06 | 40806.692620 | -46676.736613 | -16544.120931 | 5068.030397 | 23563.217104 | 40845.487542 | 58063.833664 | 76565.798203 | 98222.894111 | 128465.220975 | |

| 2011-11-07 | 43503.676450 | -46255.703438 | -15315.077993 | 6965.648074 | 25902.252457 | 43336.311215 | 61053.512552 | 80111.716545 | 102295.131332 | 133194.560977 | |

| 2011-11-08 | 39830.233893 | -51545.615185 | -20027.924158 | 2662.824619 | 21906.346012 | 39980.482428 | 58006.295602 | 77399.156839 | 99888.163672 | 131151.589197 | |

| 2011-11-09 | 36990.513044 | -56523.526649 | -24495.447993 | -1066.945972 | 18732.001915 | 37151.279157 | 55520.419680 | 75331.859267 | 98382.970785 | 130468.262942 | |

| 2011-11-10 | 42656.625332 | -52222.084277 | -19714.514788 | 3802.223665 | 23887.046793 | 42525.441250 | 61225.057142 | 81332.468161 | 104820.044505 | 137808.305522 | |

| 2011-11-11 | 44756.329828 | -52548.031615 | -18656.197064 | 5288.754038 | 25734.360637 | 44828.240961 | 63986.351020 | 84378.816506 | 108611.618683 | 142140.108263 | |

| 2011-11-12 | 37905.655743 | -60991.102805 | -27099.347751 | -2388.499412 | 18511.776221 | 38050.389629 | 57546.974229 | 78416.261580 | 102719.966853 | 136415.925032 | |

| 2011-11-13 | 44715.800505 | -55633.323514 | -20782.285358 | 3913.667987 | 24980.451031 | 44809.798552 | 64605.937576 | 85704.112222 | 110433.920792 | 144866.205041 | |

| 2011-11-14 | 38863.458282 | -62877.590928 | -28234.112477 | -2844.261356 | 18802.531926 | 38951.660430 | 59170.908563 | 80678.533877 | 105966.185779 | 141098.465744 |

Visualization

def plot_predictions(train_data, predictions, item_id, target_column, titel, ylabel):

plt.figure(figsize=(12,5))

plt.title(titel)

plt.xlabel('Date')

plt.ylabel(ylabel)

# timeseries data

y_train = train_data.loc[item_id][target_column]

plt.plot(y_train, label="Timeseries Data")

# forcast data

y_pred = predictions.loc[item_id]

plt.plot(y_pred['mean'], label="Mean Forecast")

# confidence intervals

plt.fill_between(

y_pred.index , y_pred['0.1'], y_pred['0.9'],

color='red', alpha=0.1, label='10%-90% Confidence Range'

)

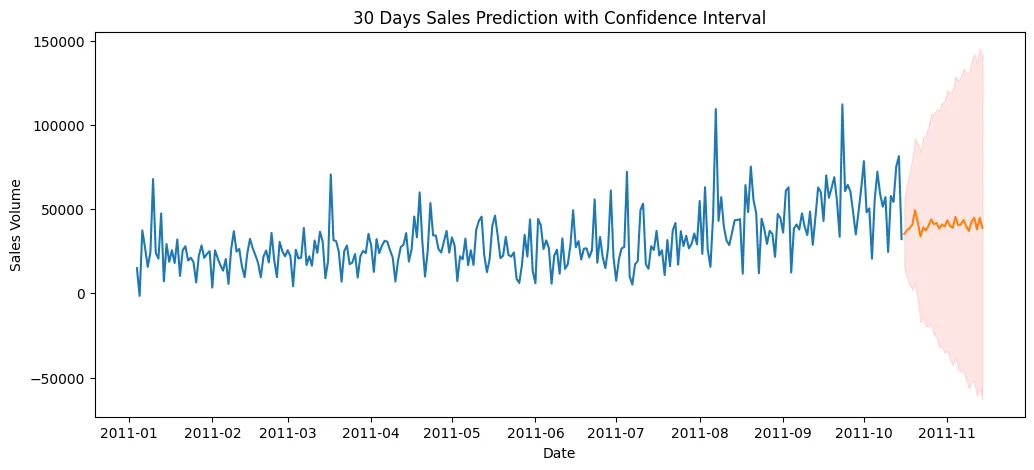

plot_predictions(

train_data, sv_predictions,

item_id='online_sales', target_column='target',

titel='30 Days Sales Prediction with Confidence Interval',

ylabel = 'Sales Volume'

)

plt.savefig('assets/AutoGluon_AutoML_TimeSeries_02.webp', bbox_inches='tight')

Multi Variate Forecasting - Future Covariants

Add known factors that affected your time series data in the past to future prediction - e.g. holidays on restaurant revenues.

# get dataset

!wget https://github.com/DaviRolim/datasets/raw/master/RestaurantVisitors.csv -P dataset

Data Preprocessing

df = pd.read_csv('dataset/RestaurantVisitors.csv')

df.tail(5)

# dataset contains unknowns -> will be used for prediction

| date | weekday | holiday | holiday_name | rest1 | rest2 | rest3 | rest4 | total | |

|---|---|---|---|---|---|---|---|---|---|

| 512 | 5/27/2017 | Saturday | 0 | na | NaN | NaN | NaN | NaN | NaN |

| 513 | 5/28/2017 | Sunday | 0 | na | NaN | NaN | NaN | NaN | NaN |

| 514 | 5/29/2017 | Monday | 1 | Memorial Day | NaN | NaN | NaN | NaN | NaN |

| 515 | 5/30/2017 | Tuesday | 0 | na | NaN | NaN | NaN | NaN | NaN |

| 516 | 5/31/2017 | Wednesday | 0 | na | NaN | NaN | NaN | NaN | NaN |

df.info()

# there are `517` entries but only `478` have a total

| Column | Non-Null Count | Dtype | |

|---|---|---|---|

| 0 | date | 517 non-null | |

| 1 | weekday | 517 non-null | object |

| 2 | holiday | 517 non-null | int64 |

| 3 | holiday_name | 517 non-null | object |

| 4 | rest1 | 478 non-null | float64 |

| 5 | rest2 | 478 non-null | float64 |

| 6 | rest3 | 478 non-null | float64 |

| 7 | rest4 | 478 non-null | float64 |

| 8 | total | 478 non-null | float64 |

df_sample = df.copy()

# renaming columns

df_sample.rename(columns={'total': 'target', 'date': 'timestamp'}, inplace=True)

df_sample['item_id'] = 'restaurant_visitors'

# get numeric representation of weekday from timestamp

datetimes = pd.to_datetime(df_sample['timestamp'])

df_sample['timestamp'] = datetimes

df_sample['weekday'] = datetimes.dt.day_of_week

# drop not needed

df_sample.drop(

['rest1', 'rest2', 'rest3', 'rest4', 'holiday_name'],

axis=1, inplace=True)

df_sample.tail(5)

| timestamp | weekday | holiday | target | item_id | |

|---|---|---|---|---|---|

| 512 | 2017-05-27 | 5 | 0 | NaN | restaurant_visitors |

| 513 | 2017-05-28 | 6 | 0 | NaN | restaurant_visitors |

| 514 | 2017-05-29 | 0 | 1 | NaN | restaurant_visitors |

| 515 | 2017-05-30 | 1 | 0 | NaN | restaurant_visitors |

| 516 | 2017-05-31 | 2 | 0 | NaN | restaurant_visitors |

# split missing data for prediction

df_sample.iloc[:478].to_csv('dataset/mv_known_series.csv', index=False)

df_sample.iloc[478:].drop('target',axis=1).to_csv('dataset/mv_unknown_series.csv', index=False)

Model Training

train_data = TimeSeriesDataFrame('dataset/mv_known_series.csv')

train_data.head(5)

| weekday | holiday | target | ||

|---|---|---|---|---|

| item_id | timestamp | |||

| restaurant_visitors | 2016-01-01 | 4 | 1 | 296.0 |

| 2016-01-02 | 5 | 0 | 191.0 | |

| 2016-01-03 | 6 | 0 | 202.0 | |

| 2016-01-04 | 0 | 0 | 105.0 | |

| 2016-01-05 | 1 | 0 | 98.0 |

# create a predictor for the length of the unknown series

mv_predictor = TimeSeriesPredictor(

prediction_length=len(df_sample.iloc[478:]),

path=MODEL_PATH,

target='target',

known_covariates_names = ['weekday', 'holiday'],

eval_metric='sMAPE'

)

mv_predictor.fit(

train_data,

time_limit=800,

presets="high_quality"

)

# Training complete. Models trained: ['Naive', 'SeasonalNaive', 'Theta', 'AutoETS', 'RecursiveTabular', 'DeepAR', 'TemporalFusionTransformer', 'PatchTST', 'AutoARIMA', 'WeightedEnsemble']

# Total runtime: 470.02 s

# Best model: WeightedEnsemble

# Best model score: -0.1501

Model Predictions

future_series = TimeSeriesDataFrame('dataset/mv_unknown_series.csv')

future_series.head(5)

| weekday | holiday | ||

|---|---|---|---|

| item_id | timestamp | ||

| restaurant_visitors | 2017-04-23 | 6 | 0 |

| 2017-04-24 | 0 | 0 | |

| 2017-04-25 | 1 | 0 | |

| 2017-04-26 | 2 | 0 | |

| 2017-04-27 | 3 | 0 |

mv_predictions = mv_predictor.predict(train_data, known_covariates=future_series, random_seed=SEED)

Visualization

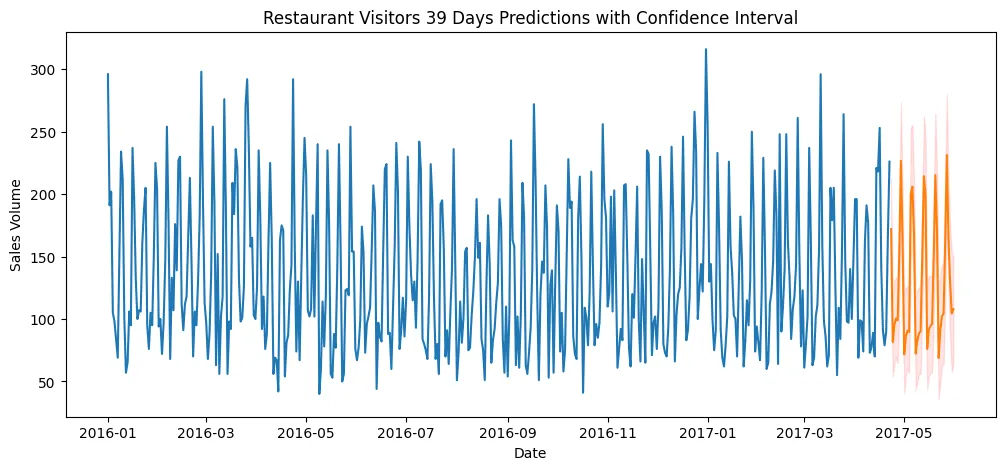

plot_predictions(

train_data, mv_predictions,

item_id='restaurant_visitors', target_column='target',

titel='Restaurant Visitors 39 Days Predictions with Confidence Interval',

ylabel = 'Restaurant Revenue'

)

plt.savefig('assets/AutoGluon_AutoML_TimeSeries_03.webp', bbox_inches='tight')

Multi Variate Forecasting - Past Covariants

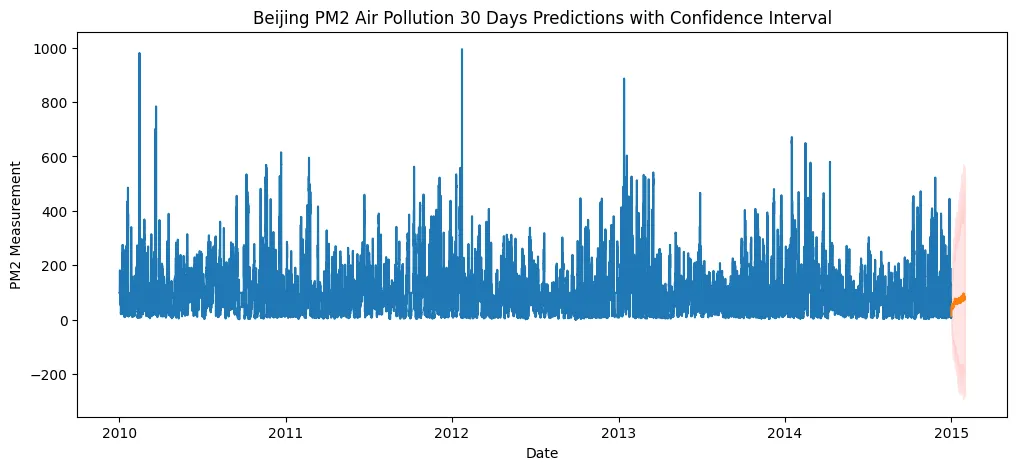

The Air Quality dataset reports on the weather and the level of pollution each hour for five years at the US embassy in Beijing, China. The data includes the date-time, the PM2.5 concentration, and the weather information including dew point, temperature, pressure, wind direction, wind speed and the cumulative number of hours of snow and rain.

# get dataset

!wget https://raw.githubusercontent.com/jyoti0225/Air-Pollution-Forecasting/master/AirPollution.csv -P dataset

Data Preprocessing

# datetime is split up into 4 columns => combine

def parse(x):

return dt.strptime(x, '%Y %m %d %H')

df = pd.read_csv('dataset/AirPollution.csv', date_parser=parse,parse_dates=[

['year', 'month', 'day', 'hour']

])

df.head(5)

| year_month_day_hour | No | pm2.5 | DEWP | TEMP | PRES | cbwd | Iws | Is | Ir | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2010-01-01 00:00:00 | 1 | NaN | -21 | -11.0 | 1021.0 | NW | 1.79 | 0 | 0 |

| 1 | 2010-01-01 01:00:00 | 2 | NaN | -21 | -12.0 | 1020.0 | NW | 4.92 | 0 | 0 |

| 2 | 2010-01-01 02:00:00 | 3 | NaN | -21 | -11.0 | 1019.0 | NW | 6.71 | 0 | 0 |

| 3 | 2010-01-01 03:00:00 | 4 | NaN | -21 | -14.0 | 1019.0 | NW | 9.84 | 0 | 0 |

| 4 | 2010-01-01 04:00:00 | 5 | NaN | -20 | -12.0 | 1018.0 | NW | 12.97 | 0 | 0 |

df.info()

# dataset contains missing pm2.5 values

# # Column Non-Null Count Dtype

# --- ------ -------------- -----

# 0 year_month_day_hour 43824 non-null datetime64[ns]

# 1 No 43824 non-null int64

# 2 pm2.5 41757 non-null float64

# 3 DEWP 43824 non-null int64

# 4 TEMP 43824 non-null float64

# 5 PRES 43824 non-null float64

# 6 cbwd 43824 non-null object

# 7 Iws 43824 non-null float64

# 8 Is 43824 non-null int64

# 9 Ir 43824 non-null int64

df_sample = df.copy()

# one-hot encode wind direction

one_hot_wind = pd.get_dummies(df['cbwd'], drop_first=True)

df_sample = pd.concat([df, one_hot_wind], axis=1, join="inner")

# renaming columns

df_sample.rename(columns={

'year_month_day_hour': 'timestamp',

'pm2.5': 'target',

'DEWP': 'dew_point',

'TEMP': 'temperature',

'PRES': 'pressure',

'NW': 'wind_direction_nw',

'SE': 'wind_direction_se',

'cv': 'wind_direction_cv',

'Iws': 'wind_speed',

'Is': 'snow',

'Ir': 'rain'}, inplace=True)

# add item_id

df_sample['item_id'] = 'pm2_pollution'

# fill missing targets with mean()

df_sample['target'] = df_sample['target'].fillna(df_sample['target'].mean())

# make datetime object

datetimes = pd.to_datetime(df_sample['timestamp'])

df_sample['timestamp'] = datetimes

df_sample['weekday'] = datetimes.dt.day_of_week

# drop not needed

df_sample.drop(['No', 'cbwd'], axis=1, inplace=True)

df_sample.head(5)

| timestamp | target | dew_point | temperature | pressure | wind_speed | snow | rain | wind_direction_nw | wind_direction_se | wind_direction_cv | item_id | weekday | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2010-01-01 00:00:00 | 98.613215 | -21 | -11.0 | 1021.0 | 1.79 | 0 | 0 | 1 | 0 | 0 | pm2_pollution | 4 |

| 1 | 2010-01-01 01:00:00 | 98.613215 | -21 | -12.0 | 1020.0 | 4.92 | 0 | 0 | 1 | 0 | 0 | pm2_pollution | 4 |

| 2 | 2010-01-01 02:00:00 | 98.613215 | -21 | -11.0 | 1019.0 | 6.71 | 0 | 0 | 1 | 0 | 0 | pm2_pollution | 4 |

| 3 | 2010-01-01 03:00:00 | 98.613215 | -21 | -14.0 | 1019.0 | 9.84 | 0 | 0 | 1 | 0 | 0 | pm2_pollution | 4 |

| 4 | 2010-01-01 04:00:00 | 98.613215 | -20 | -12.0 | 1018.0 | 12.97 | 0 | 0 | 1 | 0 | 0 | pm2_pollution | 4 |

df_sample.to_csv('dataset/bj_airpollution.csv', index=False)

Model Training

train_data = TimeSeriesDataFrame('dataset/bj_airpollution.csv')

train_data.head(5)

| target | dew_point | temperature | pressure | wind_speed | snow | rain | wind_direction_nw | wind_direction_se | wind_direction_cv | weekday | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| item_id | timestamp | |||||||||||

| pm2_pollution | 2010-01-01 00:00:00 | 98.613215 | -21 | -11.0 | 1021.0 | 1.79 | 0 | 0 | 1 | 0 | 0 | 4 |

| 2010-01-01 01:00:00 | 98.613215 | -21 | -12.0 | 1020.0 | 4.92 | 0 | 0 | 1 | 0 | 0 | 4 | |

| 2010-01-01 02:00:00 | 98.613215 | -21 | -11.0 | 1019.0 | 6.71 | 0 | 0 | 1 | 0 | 0 | 4 | |

| 2010-01-01 03:00:00 | 98.613215 | -21 | -14.0 | 1019.0 | 9.84 | 0 | 0 | 1 | 0 | 0 | 4 | |

| 2010-01-01 04:00:00 | 98.613215 | -20 | -12.0 | 1018.0 | 12.97 | 0 | 0 | 1 | 0 | 0 | 4 |

# 30-day predictor

bj_predictor = TimeSeriesPredictor(

prediction_length=24*30,

path=MODEL_PATH,

target='target',

eval_metric='sMAPE'

)

bj_predictor.fit(

train_data,

presets="high_quality"

)

# Fitting simple weighted ensemble.

# -0.8465 = Validation score (-sMAPE)

# 3.16 s = Training runtime

# 40.20 s = Validation (prediction) runtime

# Training complete. Models trained: ['Naive', 'SeasonalNaive', 'Theta', 'AutoETS', 'RecursiveTabular', 'DeepAR', 'PatchTST', 'AutoARIMA', 'WeightedEnsemble']

# Total runtime: 693.53 s

# Best model: WeightedEnsemble

# Best model score: -0.8465

Model Predictions

bj_predictions = bj_predictor.predict(train_data, random_seed=SEED)

Visualization

plot_predictions(

train_data, bj_predictions,

item_id='pm2_pollution', target_column='target',

titel='Beijing PM2 Air Pollution 30 Days Predictions with Confidence Interval',

ylabel = 'PM2 Measurement'

)

plt.savefig('assets/AutoGluon_AutoML_TimeSeries_04.webp', bbox_inches='tight')